How Do Life Insurance Companies Create Their Pricing?

- Peter C. Ciravolo

- May 25

- 4 min read

Life insurance premiums aren't chosen at random. Every policy price is based on a careful evaluation of risk, financial modeling, and long-term projections. Insurance companies must collect enough premium from policyholders to pay future claims, cover operating expenses, generate investment returns, and remain financially stable for decades.

Here's how life insurance companies determine what you'll pay.

The Foundation: Risk Assessment

At its core, life insurance pricing answers one question:

How likely is it that the insurance company will have to pay a death benefit during the policy period?

To estimate that probability, insurers evaluate several factors that influence life expectancy.

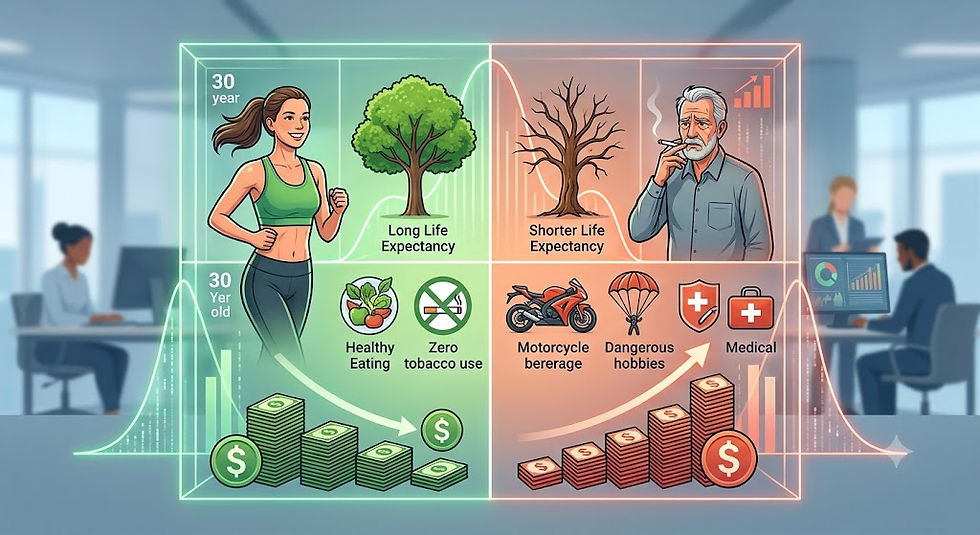

Age

Age is one of the strongest pricing factors. Statistically, younger people have a lower probability of dying in the near future than older individuals, so they generally qualify for lower premiums.

Gender

In many countries and insurance markets, women tend to have longer average life expectancies than men. Where regulations allow, this difference may result in lower premiums for female applicants.

Health History

Insurers review current health and past medical history, including:

Blood pressure

Cholesterol levels

Diabetes

Heart disease

Cancer history

Prescription medications

Applicants in excellent health generally receive more favorable pricing.

Lifestyle

Certain habits increase mortality risk, including:

Tobacco or nicotine use

Excessive alcohol consumption

Drug use

Dangerous hobbies such as skydiving or rock climbing

Riskier lifestyles often lead to higher premiums.

Occupation

Jobs involving hazardous conditions—such as construction, commercial fishing, mining, or aviation—may increase insurance costs because of the elevated risk of accidental death.

Family Medical History

A family history of conditions such as heart disease, certain cancers, or inherited disorders may affect underwriting because it can indicate elevated long-term health risks.

The Underwriting Process

Once an application is submitted, it enters underwriting.

Underwriting is the insurer's process of evaluating risk before offering coverage.

Depending on the policy, underwriting may include:

Medical questionnaires

Prescription history reviews

Medical exams

Blood and urine testing

Motor vehicle reports

Public records

Electronic health records

Consumer data and fraud screening

Some policies, particularly simplified issue or guaranteed issue life insurance, require little or no medical underwriting. Because the insurer has less information about the applicant, these products generally carry higher premiums.

Mortality Tables: Predicting Life Expectancy

Life insurers rely heavily on mortality tables.

A mortality table estimates the probability that people of a certain age and demographic profile will die during a given year.

These tables are built using millions of data points from:

Historical insurance claims

Government statistics

Population studies

Medical research

Actuaries use these tables to estimate expected claims across large groups of policyholders.

For example, if historical data suggests that 2 out of every 1,000 healthy 35-year-olds are expected to die within a year, that probability becomes one input in premium calculations.

Actuarial Science Drives the Numbers

Life insurance pricing is primarily developed by actuaries.

Actuaries use mathematics, probability, statistics, and financial modeling to estimate:

Future death claims

Expected premium income

Investment earnings

Policy lapse rates

Administrative costs

Economic conditions

Long-term profitability

Rather than focusing on one individual, actuaries analyze large populations to predict outcomes over many years.

Different Types of Policies Have Different Pricing

Not every life insurance policy is priced the same way.

Term Life Insurance

Term life covers a fixed period, such as 10, 20, or 30 years.

Pricing depends largely on:

Age

Health

Coverage amount

Length of the term

Since many term policies expire before a death benefit is paid, premiums are often lower than permanent life insurance.

Permanent Life Insurance

Whole life, universal life, and other permanent policies provide lifelong coverage if premiums are maintained.

Pricing reflects additional features, including:

Lifetime protection

Cash value accumulation

Administrative costs

Investment assumptions

Guaranteed benefits

These policies typically have higher premiums because they are designed to remain in force throughout the insured's lifetime.

Investment Income Matters

Life insurance companies don't simply hold premium payments in cash.

They invest a significant portion of premiums in assets such as:

Government bonds

Corporate bonds

Mortgages

Other conservative investments

Expected investment returns are incorporated into pricing models.

If insurers expect to earn investment income over many years, they may need to collect less premium today than if no investment income were expected.

Operating Expenses Are Included

Premiums also cover the cost of running the insurance company.

Expenses may include:

Employee salaries

Agent commissions

Customer service

Technology systems

Marketing

Policy administration

Claims processing

Regulatory compliance

Every policy contributes toward these operational costs.

Policyholder Behavior Also Affects Pricing

Insurance companies don't assume every policy will remain active forever.

Pricing models estimate behaviors such as:

Policy cancellations (lapses)

Reduced coverage

Missed premium payments

Policy loans

Early surrender of permanent policies

Understanding these patterns helps insurers better estimate future financial obligations.

Reinsurance Helps Manage Risk

Many insurers purchase reinsurance, which is essentially insurance for insurance companies.

Reinsurance allows insurers to transfer part of the financial risk associated with large policies or unusually high concentrations of risk.

The cost of reinsurance becomes another factor incorporated into premium calculations.

Regulations Influence Pricing

Life insurance pricing is subject to regulation in most jurisdictions.

Regulators review products to help ensure that premiums are:

Financially sound

Not unfairly discriminatory

Supported by actuarial analysis

Sufficient to pay future claims

Companies must also maintain adequate reserves to ensure they can meet future obligations to policyholders.

Why Two People Receive Different Quotes

Even if two applicants request the same coverage amount, they may receive very different premiums.

Differences can result from:

Age

Medical history

Tobacco use

Height and weight

Occupation

Family health history

Driving record

Policy type

Coverage amount

Policy length

Underwriting class

A healthy 30-year-old non-smoker will generally pay significantly less than a 55-year-old smoker with chronic medical conditions because their estimated mortality risk is much lower.

The Goal: Pricing That Is Fair and Sustainable

Life insurance pricing is a balance between affordability for consumers and financial sustainability for insurers. Companies combine medical underwriting, actuarial science, mortality data, expense projections, investment assumptions, and regulatory requirements to estimate the true cost of providing coverage over many years.

While the process is highly mathematical, the principle is straightforward: people who present a lower expected risk of an insurance claim generally pay lower premiums, while higher-risk applicants pay more. By accurately pricing risk across millions of policies, life insurance companies can pay claims when they're needed while remaining financially secure for future generations of policyholders.

Comments